What is Value at Risk:

- A statistical technique used to measure and quantify the level of financial risk within a firm or investment portfolio

- Parametric

- Historical Simulation

- Monte Carlo Simulation (focus)

- based on the concept of taking a current level and simulating returns of the underlying risk factors of a position instrumental model

- Considered the best practice

- More accurate than the parametric method and historical simulation method

What is Parametric Method?

- Follows Mean-Variance approach

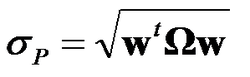

- Standard deviation of portfolio return: (equation to the left)

- where σP is the standard deviation of portfolio returns or volatility, w is the vector containing the weights of the different securities in the portfolio, Ω is the covariance matrix

What is the Historical Method?

- Does not depend on any explicit distribution of security returns

- Simulate possible returns on current portfolio using historical returns of constituent assets

- Assume the future would be similar to the past