Applications of VaR

- Equity portfolio application

- Domestic pension fund application: equities, bonds and cash

- Derivative structures

- Global portfolios: currency risk

- Hedge Funds

Strengths of VaR

- An attempt to put a single figure to the potential loss across different classes of securities

- No need to assume that manager style stays consistent over time

- VaR is the best measure available to estimate market risk in a forward-looking manner

- VaR reacts fast to changes in market risk/volatilities in the market

Weaknesses of VaR

- Indication of market fluctuations during normal market conditions

- Based on historical performance – no consideration of what the market might do in future

- A change in manager style can not be identified until enough data is collected

- Risky holdings can not be identified immediately

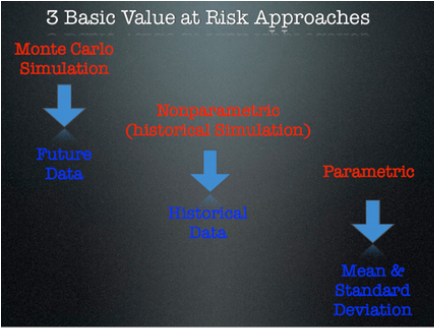

Advantages of Monte Carlo Simulation

Disadvantages of Monte Carlo Simulation

- model instruments with non-linear and path-dependent payoff functions

- not affected as much by extreme events

- can use any statistical distribution to simulate the returns as far as comfortably possible

Disadvantages of Monte Carlo Simulation

- Time consuming and complicated

- Costly to develop a VaR engine

Advantages of the Parametric Method

- Computation time is minimal

- It's simple

- It's simple

- Assumes that the historical returns and the changes in prices of the assets follow a normal distribution

- Does not cope well with securities that have a non-linear payoff like options or mortgage-backed securities

- Underestimates VaR at high confidence levels and overestimates VaR at low confidence levels

Advantages of Historical Method

- It computes quickly

- It's easy to explain to people

- Assumes the future will be similar to the past

- It produces misleading estimates

- Not easy to preform "what-if" analyses